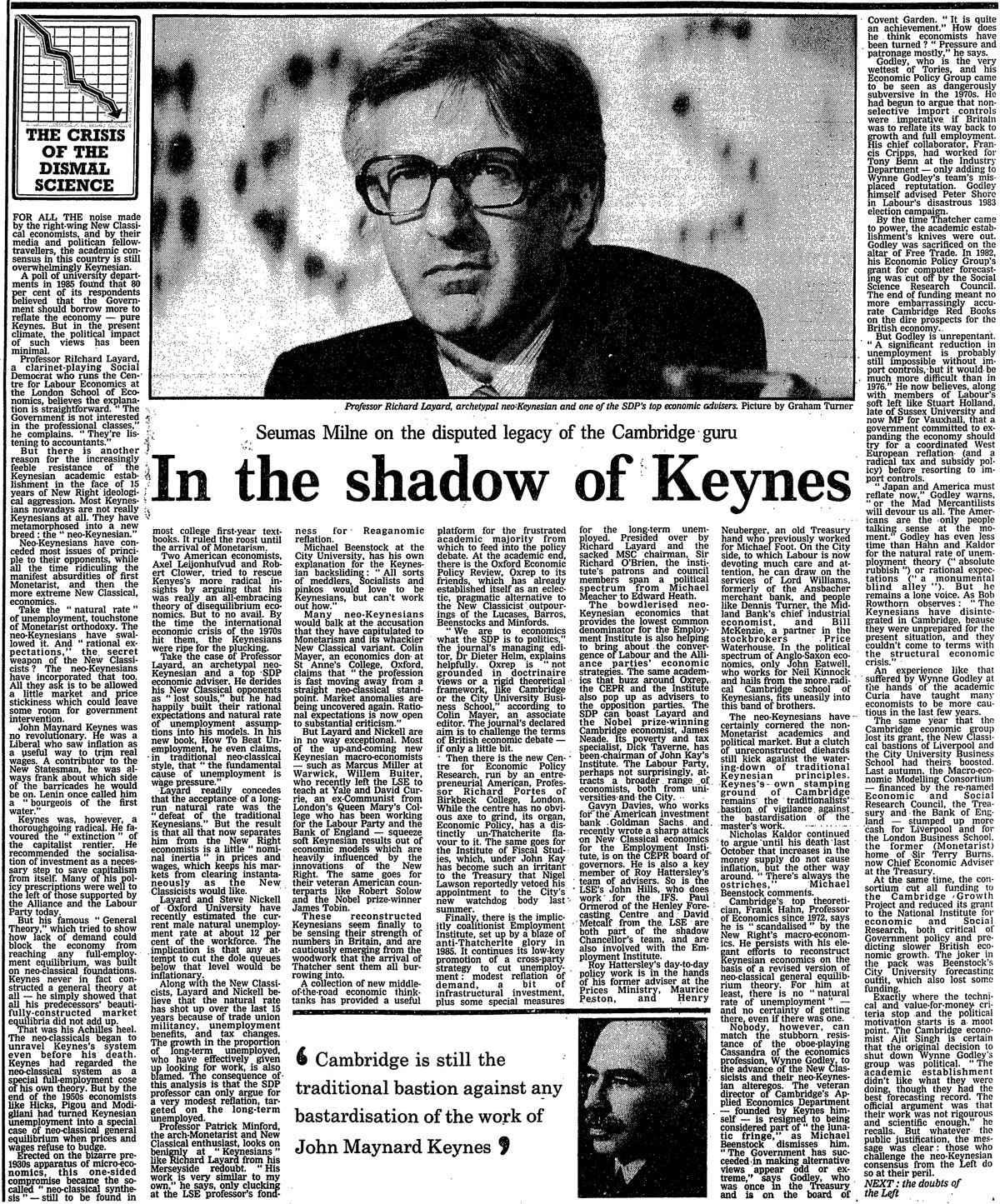

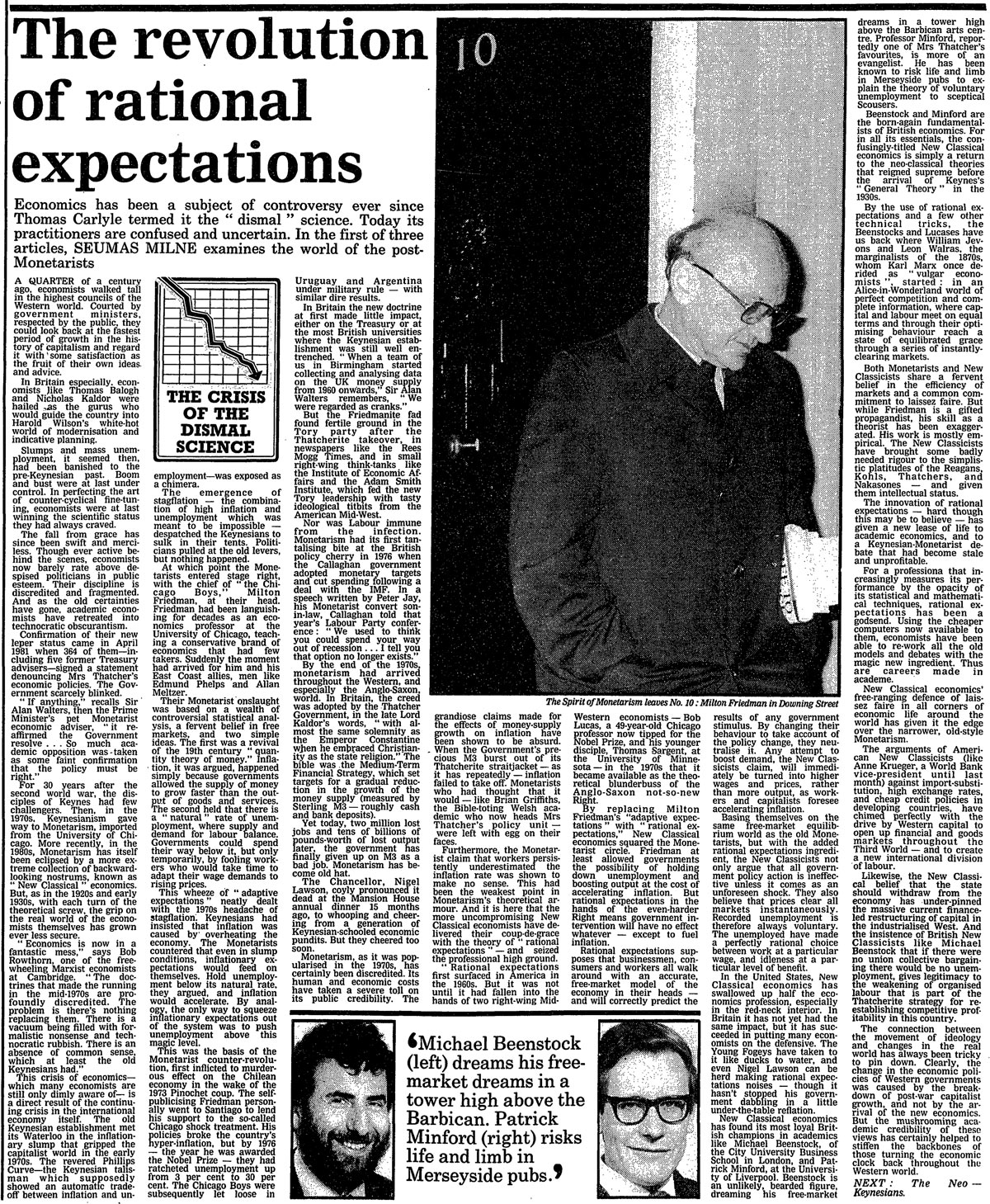

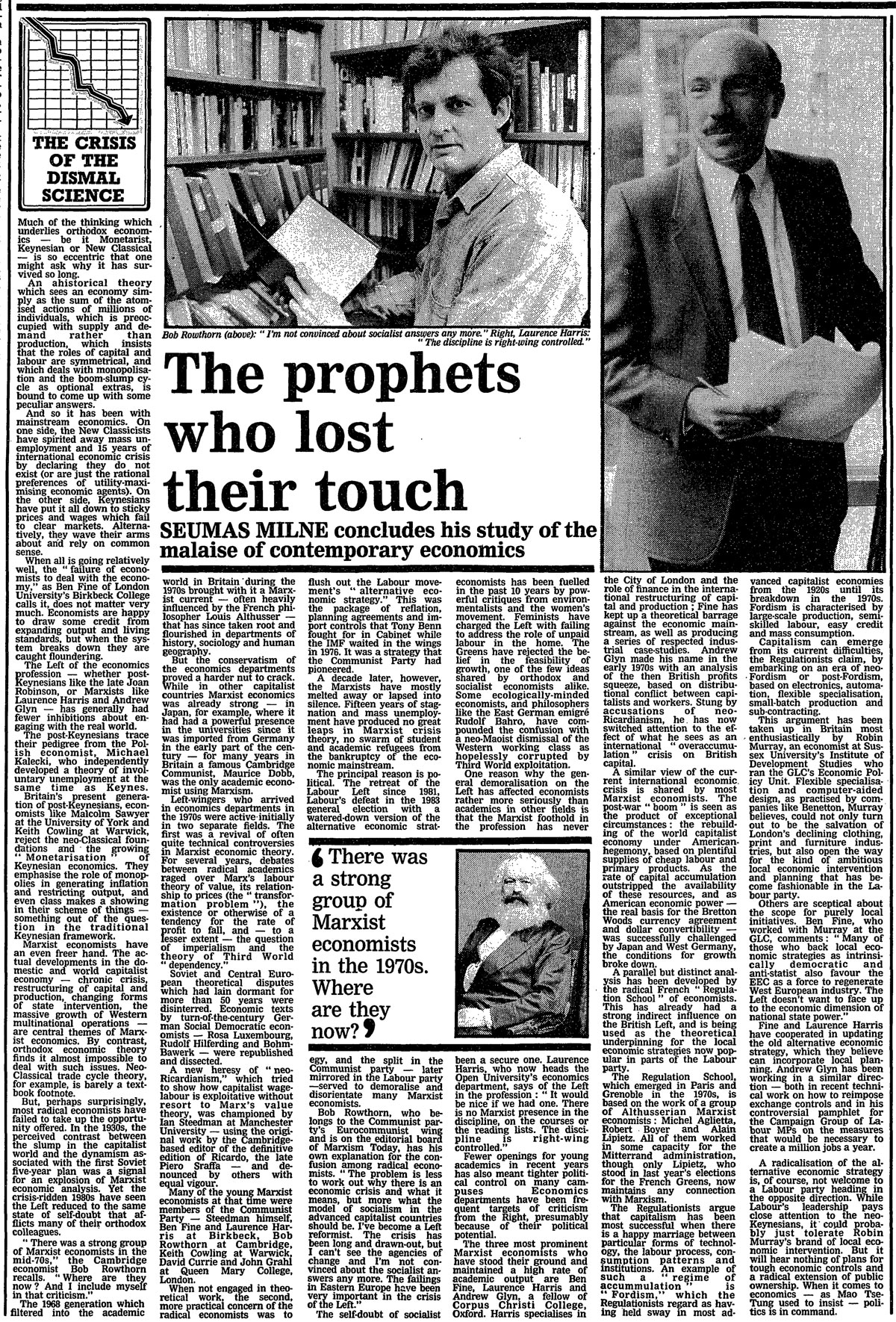

Britain's welfare spending is actually about average, while claims that it is wasteful should be seriously challenged

Labour support for the welfare bill lies in the fact it 'exempts “cyclical” spending, such as unemployment benefit'. Photograph: Matt Cardy/Getty Images

With Labour voting for the government's bill to cap welfare spending, the debate on the welfare state has taken a decisively wrong turn. The issue is not the cap itself, its level, or even its design. The problem lies in the very way in which the welfare state is understood.

Even if one accepts the need for the cap, there are many problems with the way in which it is designed. Many people have rightly pointed out that the capping scheme is not as "recession proof" as it is portrayed. One defence of the bill offered by the government – and accepted by Labour as the key justification for its support – is that it exempts "cyclical" spending, such as unemployment benefit (now given the Orwellian name jobseekers' allowance). But there are other elements of welfare spending that increase in economic downturns that won't be exempt. For example, recessions may increase the need for disability benefit because more people are incapacitated due to the psychological and physical impact of unemployment, poor diet, and lack of heating.

The need for disability benefit can also be increased by an ageing population, which is one of the structural factors that are not recognised by the bill and drive up the costs of certain elements of welfare spending. It has also been pointed out that capping could be a false economy because it may increase the demands for other public services, such as education and social services, that are not covered by the bill.

Important though these criticisms are, the biggest issue is the very way in which the "problem" of the British welfare state has been defined and understood. The cap is based on the view that the UK needs "to prevent welfare costs spiralling out of control", given the wasteful nature of such spending. This is not backed up by the evidence.

The British, having supposedly invented the modern welfare state (a debatable proposition), have the mistaken notion that they have an exceptionally generous welfare state, as evidenced by the widespread worries about "welfare scrounging" and "welfare tourism". However, measured by public social spending (eg income support, pensions, health) as a proportion of GDP, Britain's is not much bigger than the OECD average; 24.1% against 22.1% as of 2009. And the OECD includes among its 34 members a dozen or so relatively poor economies – Mexico, Chile, Turkey, Estonia and Slovakia, for example – where the welfare state is much smaller for various reasons (eg younger population, weaker parties of the left).

Even when it comes to income support for the working-age population – the element targeted by the new bill – the UK is not a particularly generous place. In 2007 it spent 4.5% of GDP for the purpose. This was only slightly above the OECD average (3.9%) and way below other rich European economies: the figures were 7.2% for Belgium, 7% for Denmark, 6% for Finland and 5.6% for Sweden.

And it is not even as if the need for social spending goes away if you reduce the welfare state. For many British supporters of a smaller welfare state the role model is the US, which has a very small welfare state (considering its level of income), accounting for only 19.2% of GDP as of 2009. However, it has a huge level of private spending on social expenditure, especially medical insurance and private pensions, which is equivalent to 10.2% of GDP. This means that, at 29.4%, the US has total social spending that is almost as high as that of Finland, which spends 30.7% of GDP on it (29.4% public and 1.3% private). Moreover, if the cost is "spiralling out of control" anywhere, it is in the largely private US healthcare system, thanks to over-treatment of patients, rising insurance premiums and soaring legal costs.

Most importantly, the view that social spending is wasteful needs to be seriously challenged. The frequently used argument against the welfare state is that it reduces economic growth by making the poor workshy and the rich reduce their wealth creation, given the tax burden involved.

However, there is no general correlation between the size of the welfare state and the growth performance of an economy. To cite a rather striking example, despite having a welfare state that is 50% bigger than that of the US (29.4% of GDP as against 19.2% of GDP in the US, in 2009), Finland has grown much faster. Between 1960 and 2010 Finland's average annual per capita income growth rate was 2.7%, against 2% for the US. This means that during this period US income rose 2.7 times while Finland's rose by 3.8 times.

The point is that the welfare state – if well designed and coordinated with labour market policies to re-train people and get them back into work – can encourage people to be more accepting of change, thereby promoting growth. Firms in countries such as Finland and Sweden can introduce new technologies faster than their US competitors because, knowing that unemployment need not mean penury and long-term joblessness, their workers do not resist these changes strongly.

Most American workforces are not organised and thus incapable of resisting technological changes that create unemployment – but the minority that are organised, such as the automobile workers, resist them tooth and nail because they know that if they lose their jobs, they will not even be able to afford to go to hospital, and will find it extremely difficult to get back into the labour market at the same level.

The British debate on the welfare state needs to be recast. The false premise that the country has a particularly generous welfare state whose cost is spiralling out of control needs to be abandoned. The structural factors driving up welfare costs, such as ageing, should be accepted – rather than denied and so putting undue pressure on other elements of social services.

Above all, the debate should be redirected into reforming the welfare state in a way that promotes structural change and economic growth.

{kind=link}

{kind=link}

{kind=link}